Securing Their Future: A Guide to Special Needs Planning

More Than a Plan—It's Peace of Mind

As a parent or guardian of a loved one with special needs, you are their fiercest advocate and their greatest champion. You’ve dedicated yourself to ensuring they have every opportunity to thrive. But one question often weighs heavily on the heart: “What happens when I’m no longer here to protect them?”

Special needs planning is the answer to that question. It’s not just about legal documents; it’s about creating a comprehensive life plan that protects your loved one’s quality of life, preserves their eligibility for essential government benefits, and ensures they are cared for by people they trust. My role is to walk alongside you in this journey, transforming your worries into a concrete, legally sound strategy that provides a lifetime of security.

Common Myths vs. Crucial Realities

Navigating the world of special needs planning can be confusing, and misinformation is common. Let's clear up some of the biggest myths to protect your loved one's future.

| The Myth | The Reality |

|---|---|

|

"I can just leave money to my child in my will."

One of the most dangerous misconceptions

|

Why This Can Destroy Their Benefits

A direct inheritance, even a small one, can be counted as an asset that disqualifies your child from vital means-tested government benefits like Medicaid and Supplemental Security Income (SSI), which cover housing, healthcare, and essential therapies. Without proper planning, your gift of love could inadvertently strip away the very support systems your child depends on.

|

|

"My other children will take care of their sibling."

Good intentions aren't legal protection

|

The Burden This Places on Families

While their intentions are good, this places an enormous and often unfair moral and financial burden on your other children. It also offers no legal protection. A formal plan ensures that designated funds are used specifically for your child with special needs and are managed by a chosen trustee, preventing family disputes and financial strain while protecting sibling relationships.

|

|

"A standard trust is good enough."

Not all trusts are created equal

|

The Special Needs Trust Difference

A generic living trust does not contain the specific, complex legal language required by federal law to protect benefit eligibility. Only a properly drafted Special Needs Trust (SNT) is designed to supplement, not replace, government benefits, allowing the funds to be used for quality-of-life enhancements without jeopardizing their essential support systems.

|

|

"Guardianship is automatic when my child turns 18."

Legal adulthood doesn't consider disability

|

The Guardianship Reality

At age 18, your child is legally considered an adult, regardless of their disability. You will no longer have the automatic right to make medical or financial decisions for them. You must petition the probate court to be appointed as their legal guardian to continue making these critical decisions. This process should be started well before their 18th birthday to ensure continuity of care.

|

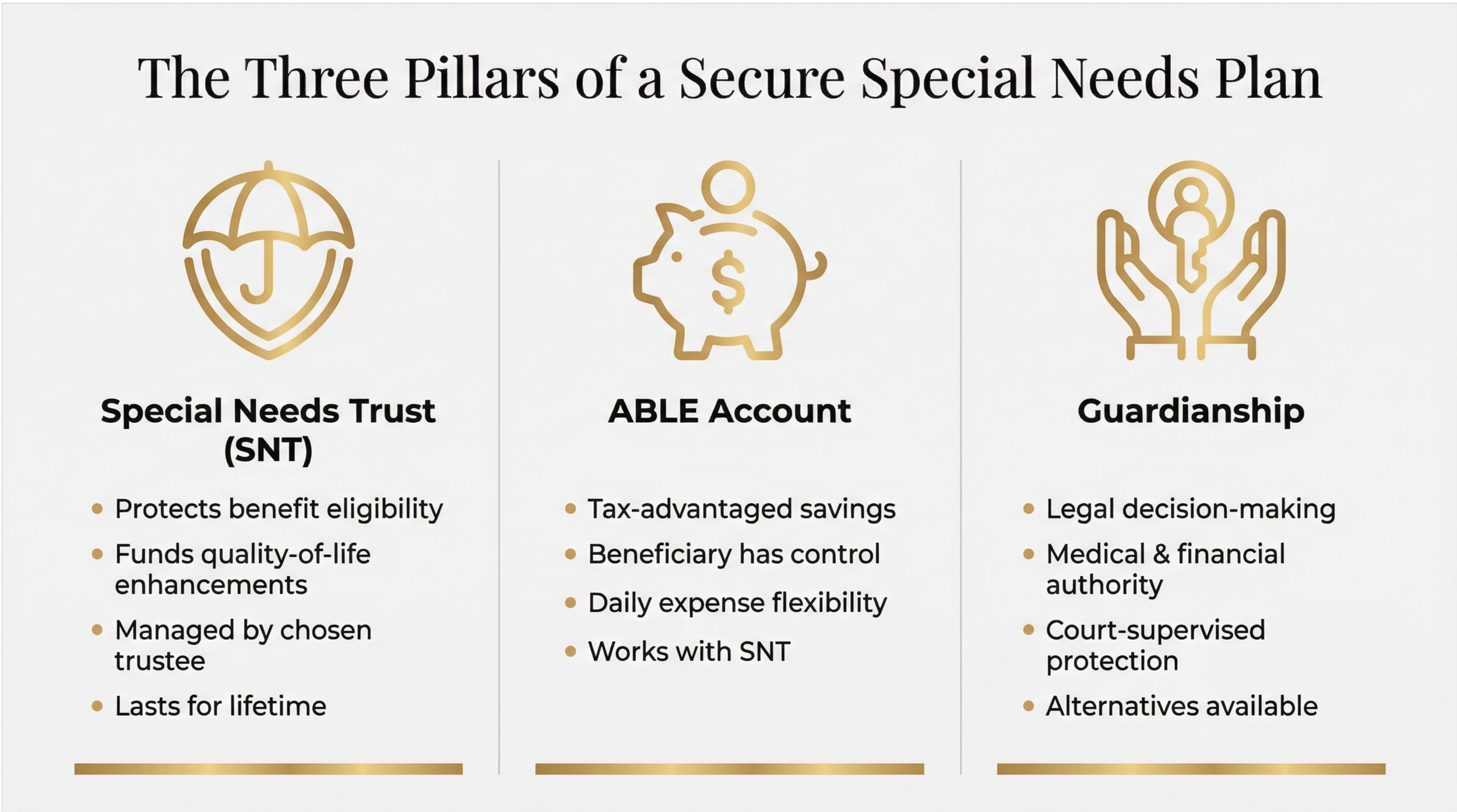

The Three Pillars of a Secure Special Needs Plan

A comprehensive plan is built on three essential legal tools working in harmony.

The Special Needs Trust (SNT)

1

This is the cornerstone of your plan. An SNT is a specialized legal document that holds assets for the benefit of your loved one. Because the assets are owned by the trust—not the individual—they don’t count against eligibility for government benefits.

What can trust funds be used for? Anything that enriches your loved one’s life: education, recreation, hobbies, travel, specialized equipment, a vehicle, and out-of-pocket medical or dental care.

Who manages the trust? You will appoint a trustee (a person or financial institution) who is responsible for managing the funds and making distributions according to your wishes.

The ABLE Account

2

An ABLE (Achieving a Better Life Experience) account is a tax-advantaged savings account that, like an SNT, allows individuals with disabilities to save money without losing their government benefits. It offers more flexibility for certain daily expenses.

Key Benefit: The beneficiary can have more direct control over the funds for day-to-day expenses, fostering independence.

How it works with an SNT: An SNT can make distributions into an ABLE account, giving the beneficiary a degree of financial freedom while the bulk of the assets remain protected in the trust.

Guardianship (or Alternatives)

3

When your child turns 18, you may need to establish legal guardianship to continue making decisions on their behalf.

What is Guardianship? A court-supervised process where a guardian is appointed to make personal, medical, and financial decisions for an individual who is unable to make them on their own.

Are there alternatives? For individuals with higher functional capacity, less restrictive options like a Healthcare Power of Attorney or Financial Power of Attorney may be appropriate. We will explore the solution that best fits your loved one’s unique situation.

A Plan Built on Compassion and Experience

I understand that this process is deeply personal. It’s about family, love, and legacy. I am committed to listening to your story, understanding your hopes for your child’s future, and translating them into a legal plan that works. You don’t have to navigate this alone.

Ready to build their safety net?